Understanding why a hard inquiry impacts your credit score is crucial for anyone looking to maintain or improve their financial health. A hard inquiry occurs when a lender checks your credit report to assess your creditworthiness. While it might seem like a routine process, this action can have a lasting effect on your credit score. In this article, we’ll explore the reasons behind this impact, how long it lasts, and what you can do to mitigate its effects.

Many people are unaware of the nuances of credit inquiries and how they influence their credit score. This lack of awareness can lead to unintentional missteps that harm their financial standing. By understanding the mechanics of hard inquiries, you can take proactive steps to protect your credit health.

In this guide, we’ll delve into the specifics of hard inquiries, their effects on credit scores, and strategies to minimize their impact. Whether you’re applying for a loan, a credit card, or any other financial product, knowing how these inquiries work will empower you to make informed decisions.

Read also:Michael Keatons Movie Career A Comprehensive Look At What Movies Did Michael Keaton Play In

Table of Contents

- What Is a Hard Inquiry?

- Hard vs. Soft Inquiries

- Why Does a Hard Inquiry Affect Credit?

- How Much Does a Hard Inquiry Lower Your Score?

- How Long Does a Hard Inquiry Stay on Credit Report?

- Types of Hard Inquiries

- Mitigating the Impact of Hard Inquiries

- Strategies to Avoid Excessive Hard Inquiries

- Common Misconceptions About Hard Inquiries

- Frequently Asked Questions

What Is a Hard Inquiry?

A hard inquiry occurs when a lender pulls your credit report to evaluate your creditworthiness for a loan, credit card, or other financial product. Unlike soft inquiries, which do not affect your credit score, hard inquiries leave a mark on your credit report and can impact your credit score.

Hard inquiries are typically initiated by you when you apply for credit. For instance, when you apply for a mortgage, auto loan, or personal loan, the lender will conduct a hard inquiry to assess your financial history and determine the risk of lending to you.

It’s important to note that not all credit checks result in a hard inquiry. For example, pre-approval offers or background checks for employment purposes generally involve soft inquiries, which do not affect your credit score.

Hard vs. Soft Inquiries

Understanding the difference between hard and soft inquiries is essential for maintaining your credit health. Here’s a breakdown of the two:

Hard Inquiries

- Initiated by you when applying for credit

- Visible to lenders on your credit report

- Can impact your credit score

- Typically remain on your credit report for two years

Soft Inquiries

- Initiated without your direct involvement (e.g., pre-approval offers)

- Not visible to lenders

- Do not affect your credit score

- Used for informational purposes only

Knowing the distinction between these two types of inquiries can help you avoid unnecessary damage to your credit score.

Why Does a Hard Inquiry Affect Credit?

Credit scoring models, such as FICO and VantageScore, consider hard inquiries as potential indicators of financial risk. When you apply for credit, it may signal that you are taking on additional debt, which could increase your financial burden. Lenders view multiple hard inquiries within a short period as a red flag, as it may indicate financial distress or excessive borrowing.

Read also:What Is Vertical Labret A Comprehensive Guide To This Unique Piercing

However, not all hard inquiries are treated equally. For example, rate shopping for a mortgage or auto loan is recognized by credit scoring models, and multiple inquiries within a 14-45 day window are grouped together and counted as a single inquiry. This exception helps consumers shop for the best rates without unfairly penalizing their credit score.

Ultimately, the impact of a hard inquiry depends on your overall credit profile. If you have a strong credit history with a long track record of responsible borrowing, the effect may be minimal. On the other hand, if you have a limited credit history or a history of missed payments, the impact could be more pronounced.

How Much Does a Hard Inquiry Lower Your Score?

The impact of a hard inquiry on your credit score varies depending on several factors, including your credit history and the credit scoring model used. On average, a single hard inquiry can lower your credit score by 5-10 points. While this may seem significant, the effect is typically temporary and diminishes over time.

For individuals with a high credit score, the impact may be more noticeable, as there is less room for fluctuation. Conversely, those with a lower credit score may experience a smaller impact, as their score already reflects a higher level of risk.

It’s important to note that the effect of a hard inquiry is cumulative. If you have multiple hard inquiries in a short period, the impact on your credit score could be more substantial. This is why it’s crucial to apply for credit sparingly and strategically.

How Long Does a Hard Inquiry Stay on Credit Report?

A hard inquiry remains on your credit report for two years. However, its impact on your credit score typically diminishes after the first year. Credit scoring models place more weight on recent activity, so older inquiries have less influence on your score.

While the presence of a hard inquiry on your credit report may concern some borrowers, it’s important to remember that it’s just one of many factors that contribute to your overall credit score. By maintaining a strong credit history and practicing responsible financial habits, you can minimize the long-term impact of hard inquiries.

Additionally, some credit scoring models, such as the newer versions of FICO and VantageScore, may exclude hard inquiries that are older than 12 months when calculating your score. This means that the impact of a hard inquiry may be even shorter-lived than the two-year reporting period suggests.

Types of Hard Inquiries

Hard inquiries can occur in various scenarios, depending on the type of credit product you’re applying for. Here are some common examples:

- Mortgage Inquiries: When applying for a home loan, lenders conduct a hard inquiry to assess your creditworthiness.

- Auto Loan Inquiries: Similar to mortgage inquiries, auto loan applications involve hard inquiries to evaluate your financial history.

- Credit Card Applications: Each time you apply for a new credit card, a hard inquiry is recorded on your credit report.

- Personal Loan Applications: Hard inquiries are also common when applying for personal loans or lines of credit.

- Student Loan Applications: Borrowing for education purposes often involves a hard inquiry to determine eligibility and interest rates.

Understanding the types of hard inquiries can help you anticipate their impact and plan accordingly.

Mitigating the Impact of Hard Inquiries

While hard inquiries are unavoidable in certain situations, there are steps you can take to minimize their impact:

1. Rate Shopping

As mentioned earlier, rate shopping for mortgages or auto loans is recognized by credit scoring models. By limiting your inquiries to a specific time frame (usually 14-45 days), you can group multiple inquiries into a single event, reducing their impact on your credit score.

2. Pre-Qualify Before Applying

Many lenders offer pre-qualification options that involve soft inquiries. This allows you to assess your eligibility and compare offers without affecting your credit score.

3. Limit Credit Applications

Avoid applying for multiple credit products in a short period. Each application results in a hard inquiry, which can compound the impact on your credit score.

4. Monitor Your Credit Report

Regularly reviewing your credit report can help you identify unauthorized hard inquiries and take action to dispute them if necessary.

Strategies to Avoid Excessive Hard Inquiries

Excessive hard inquiries can signal financial instability to lenders, making it harder to secure favorable terms on loans or credit cards. Here are some strategies to avoid unnecessary inquiries:

- Research Before Applying: Understand the credit requirements for a product before submitting an application.

- Focus on Pre-Approval Offers: Take advantage of pre-approval offers, which often involve soft inquiries.

- Limit Credit Card Applications: Avoid applying for multiple credit cards within a short period, as each application results in a hard inquiry.

- Use Credit Monitoring Tools: Leverage free credit monitoring tools to track your credit health and avoid unnecessary inquiries.

By adopting these strategies, you can protect your credit score and maintain a healthy financial profile.

Common Misconceptions About Hard Inquiries

There are several misconceptions surrounding hard inquiries that can lead to confusion and misinformation. Here are some common myths debunked:

1. All Credit Checks Are Hard Inquiries

Fact: Not all credit checks result in hard inquiries. Soft inquiries, such as those for pre-approval offers or employment background checks, do not affect your credit score.

2. Hard Inquiries Have a Permanent Impact

Fact: While hard inquiries remain on your credit report for two years, their impact diminishes over time and typically disappears after the first year.

3. Checking Your Own Credit Hurts Your Score

Fact: Checking your own credit report involves a soft inquiry, which does not affect your credit score. In fact, monitoring your credit is a responsible financial practice.

By understanding these misconceptions, you can make informed decisions about your credit health.

Frequently Asked Questions

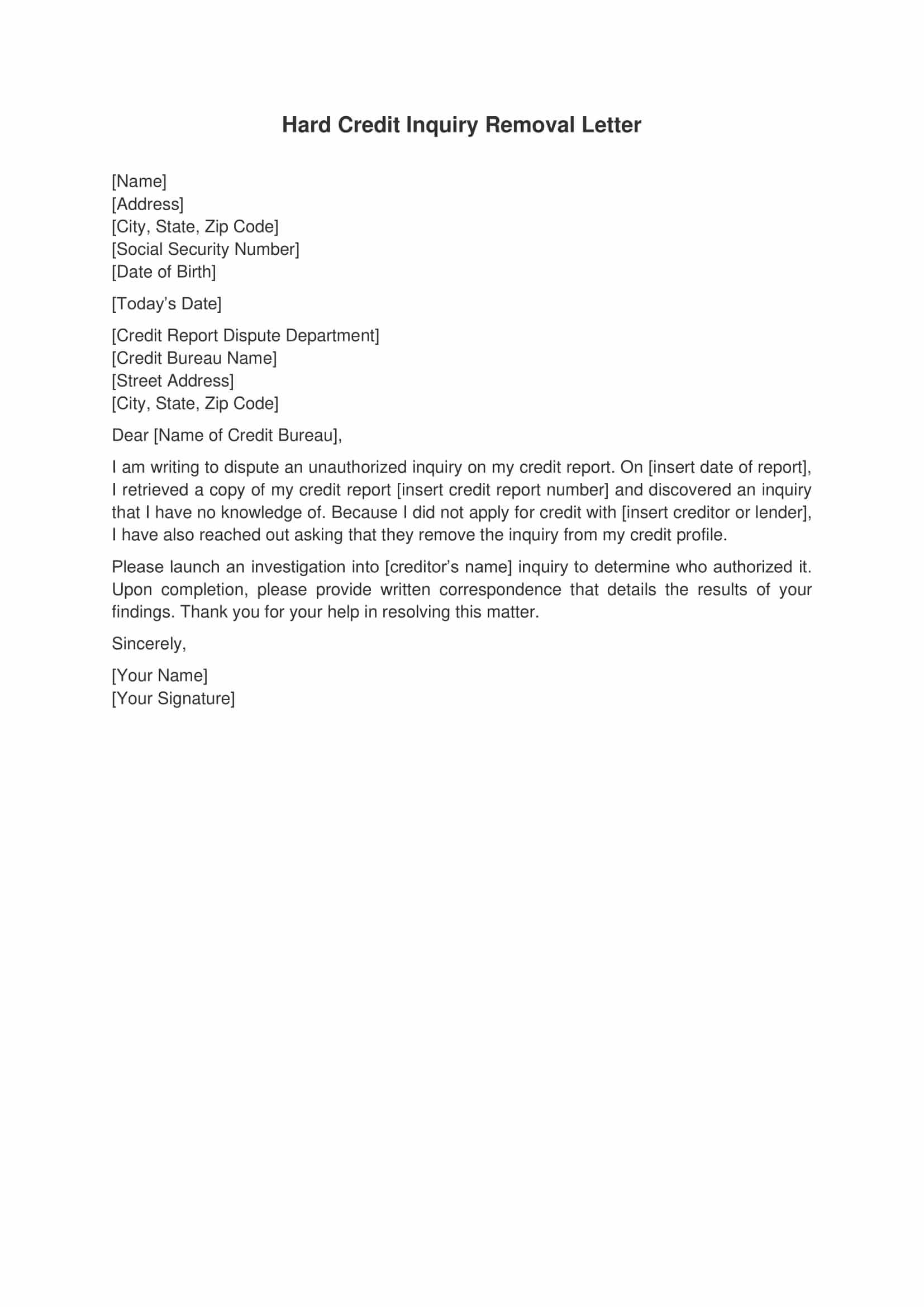

1. Can a Hard Inquiry Be Removed From My Credit Report?

Unauthorized hard inquiries can be disputed and removed from your credit report. If you notice an inquiry you didn’t initiate, contact the credit bureau to file a dispute.

2. How Many Hard Inquiries Are Too Many?

There is no specific number of hard inquiries that is considered too many. However, applying for multiple credit products in a short period can raise red flags for lenders and negatively impact your credit score.

3. Do Hard Inquiries Affect All Credit Scores Equally?

No, the impact of hard inquiries varies depending on your overall credit profile. Individuals with a strong credit history may experience a smaller impact compared to those with a limited or poor credit history.

Conclusion

In summary, hard inquiries can have a temporary impact on your credit score, but their effect diminishes over time. By understanding how hard inquiries work and taking proactive steps to minimize their impact, you can maintain a healthy credit profile and achieve your financial goals.

We encourage you to share your thoughts and experiences in the comments below. Additionally, feel free to explore other articles on our site for more insights into credit management and financial wellness. Together, let’s build a brighter financial future!

Data sources and references: